Business

VA Construction Loans | Requirements & Process 2022

You may have heard that VA construction loans can be challenging to find. Many VA lenders do not offer them.

VA construction loans are available to qualified veterans and active-duty service members. Pay for home construction costs. Borrowers can often build their dream homes with little money down.

Despite this, not everyone can benefit from a VA construction loan. A VA home purchase loan is more straightforward for many military personnel.

Read More: Alternatives To Construction Loans

Compare personalized rates from multiple lenders to get a quote. Begin here (Dec 5, 2022).

What’s a VA Construction Loan?

You can buy land and build your home with one loan through VA construction.

The traditional construction loan consists of three loans that cover the following:

- Land acquisition costs – The first loan is to purchase the land you will build.

- Home construction costs – The second pays construction costs in stages as your home builds.

- Permanent loan – This third loan is used to repay the two previous short-term loans. It then acts as a long-term mortgage loan for your home with monthly mortgage payments.

A VA construction loan is a single loan that can replace three loans. Purchase the land or pay the construction costs in stages as your contractor progresses.

Once your home is completed, you won’t need a new mortgage. Your VA loan is already in effect.

It is a beautiful idea. It’s a great idea if you can find one.

How do I get a VA loan for a new construction project?

You must qualify for the VA loan program to use a VA home loan for new construction.

VA loan benefits are available to most active duty, retired, and honorably discharged service personnel.

Before you proceed to the next step, make sure you check the eligibility requirements.

Step 1: Locate a lender offering VA construction loans.

The U.S. Department of Veterans Affairs doesn’t lend money to homebuilders or homebuyers. Instead, the U.S. Department of Veterans Affairs authorizes private lenders to provide VA-insured loans for eligible vets.

Many VA mortgage lenders are available to homebuyers, but finding a lender to provide a VA construction loan takes time and effort.

Below is a listing of mortgage companies offering construction loans.

Editor’s note: These companies are not affiliated with us, and we have not evaluated them. Before contacting anyone, do your research.

- Wholesale: American Financial Resources can be used as a wholesale lender, meaning you cannot borrow directly from them. You will need to find a wholesale mortgage company using this wholesaler. AFR Wholesale claims it can provide 100% financing for construction loans. It requires a minimum of 620 credit score, and there are no monthly payments during construction.

- Security America Mortgage: The Texas-based lender offers 100% financing with no monthly payments.

- VA Nationwide Home Loans: These are divisions of Magnolia Bank. These loans are 100% financing, with a minimum credit score of 620, and fund the construction phase.

These are your choices.

Step 2: Get your Certificate Of Eligibility

You will need your Certificate of Eligibility (from the Department of Veterans Affairs) to be eligible for any VA loan, including the VA construction loan. This document proves that you are eligible for VA home loan benefits.

You can apply to a COE or ask your loan officer for assistance.

Step 3: Get preapproved for your price range

Pre-approval could be a rehearsal for your loan application. You can be preapproved by a VA-authorized loan lender and apply for the actual loan.

Pre-approval is similar to a loan application. It will consider your debt-to-income ratio, credit score, income stability, and down payment amount if you choose one.

Pre-approval will give you an advantage when applying for a mortgage. It will show you how much money you can borrow and your monthly mortgage payments and mortgage rate. It will also show your builder that you can afford the construction costs.

Step 4: Locate a VA-approved homebuilder

Once approved for a VA construction loan, it is time to start looking for your home’s builder. The Department of Veterans Affairs must approve the builder.

This form allows you to search for builders near you. To ensure you work with someone you can trust and who communicates well, speak to at least three builders. You should ensure that the builder is familiar with the type and style of home you want.

The VA will not allow you to complete the work even if you are a licensed contractor, home builder, or architect.

Your builder will need to assume more financial responsibility with the VA program. Additionally, they will need to provide a warranty. Before you spend too much time talking to builders, ensure they understand what you are getting. It’s best to give them the VA’s short overview of what’s involved.

Step 5: Get the OK of an appraiser.

Now that you have both a lender and a builder in mind, it is time to start sketching out your ideas. Before you can get the loan approved, make sure you have your plans in order.

Your loan officer should contact the appraiser to plan the appraisal process. The appraiser cannot simply visit the home and take notes since the house has yet to be available. The appraiser will need to determine the projected value of the home based on its plans.

You may need to revise plans if the appraiser believes your home is not worth the construction costs. You may also find a better lot, as the location impacts real estate value.

Step 6: Close your loan and get started building

You can apply for a loan by getting the VA approval for your builder and building plans.

The loan underwriting process can take anywhere from four to six weeks. The lender will not issue a lump sum of cash as with a purchase loan once the loan is closed. Instead, the lender will distribute funds slowly according to your draw schedule.

Fast loans mean that the builder can use the money as necessary.

Step 7: Get your VA-approved home completed.

After completing your home, the VA will inspect it again to ensure it meets the minimum property requirements. Your home should pass inspection easily because it is brand new. It assumes that the builder adhered to local building codes.

The VA has approved the construction.

VA construction loan requirements

You must be a qualified borrower to get a VA construction loan. Your builder and project must also meet the VA requirements.

Borrowers’ requirements

Whether you are a veteran or active-duty military servicemember with a Certificate of Eligibility, it won’t take too long to meet the VA’s requirements.

The VA doesn’t have any strict underwriting requirements. However, VA lenders can have a higher standard. For construction loans, most VA lenders require credit scores of at least 640.

Your lender will use your debt-to-income ratio to determine your construction loan amount. Lenders prefer a balance between 41% and 51%.

Depending upon your entitlement, you will also need to pay an upfront VA funding fee, ranging from 2.3% to 3.6%. The price is lower for first-time borrowers. However, this is a significant expense in your loan amount. It also means you don’t need private mortgage Insurance (PMI).

Builders’ requirements

Builders on VA-financed construction projects are more accountable than those financed with conventional loans. Builders are responsible for closing costs. However, they may be able to negotiate these into your building expenses.

The VA maintains a list of approved contractors. There are many options, as the list is extensive in many areas. If you need to be connected with VA-approved builders, your loan officer can help.

You will likely need a conventional loan if you want to work with a non-VA builder.

Project requirements

The Department of Veterans Affairs covers only home loans for primary residences. The government agency wants home finances to be safe, affordable, and well-suited for their residents.

The VA will assign an appraiser to review your plans and help you reach this goal. If an appraiser determines your home is not worth the construction cost, you must amend your plans.

The appraiser will verify that the property meets the VA’s Minimum Properties Requirements.

Is it challenging to obtain a VA construction loan?

Lenders are required to accept greater risk when lending construction loans. It makes them more challenging to obtain.

Lenders are more cautious with these loans because the house you’re financing isn’t yet available. A purchase loan allows the lender to recoup losses by selling your home if you default.

Construction loans are only available once your home is completed. If you are applying for a construction loan, expect the loan officer to ask only a few questions. Don’t be surprised if they want to see a higher credit score than traditional VA mortgages.

The VA will only guarantee a portion of your VA construction loan. Private lenders are what you’re borrowing. Private lenders have the right to establish their standards and requirements above and beyond those of the VA.

A VA construction loan is still more accessible than a conventional loan. Finding a lender that offers a VA loan is the most challenging part for some borrowers.

VA construction loan vs. traditional construction loan

A VA construction loan is available to veterans eligible for a VA loan. It does not require any collateral. You can borrow money without:

- You may need an initial down payment if you have a VA loan.

- Private Mortgage Insurance (PMI) – To avoid conventional mortgage insurance, you’d need 20% down. No matter how large your down payment, USDA and FHA loans will require mortgage insurance. VA loans only require the upfront VA funding fee.

- VA loan limits – You can borrow as much as your lender approves. There is no limit to the VA’s loan size.

- Geographical requirements – Unlike USDA loans, VA loans work in all parts of the U.S.

- Income requirements – Unlike USDA loans, you can still use your VA loan benefits, regardless of how much you earn.

This deal is not available with conventional loans.

What’s the deal with the VA construction loan, you ask? These loans are difficult to find as only a few VA lenders offer them.

You may need to look for another type of loan if you are still looking for a lender who will also underwrite VA construction loans.

Alternatives to a VA Construction Loan

If you are having trouble finding a lender who offers VA construction loans, there may be other options.

Conventional loans are the obvious choice. For construction costs and buying land, you may require separate loans. A significant down payment will likely be necessary for one or both loans.

Another option is to obtain a “one-time close mortgage” backed by Federal Housing Administration (FHA). It is similar to a VA construction loan.

There are some drawbacks.

- FHA requires that a minimum down payment of 3.5% be made on the loan amount

- After you pay your mortgage, you will have to pay monthly mortgage insurance.

You can refinance an FHA loan to a VA loan as soon as the home is finished. You can also refinance 100% to get your FHA down payment back.

For general inquiries:

* Email: sales@commerciallendingusa.com

* Phone: +1 (571) 544-6600

Amazon courtesy credit, the e-commerce giant, is known for its customer-centric approach and commitment to ensuring a satisfactory shopping experience for its users. One of the ways Amazon achieves this is through its CC policy, aimed at compensating customers for certain inconveniences or issues encountered during their shopping journey.

What is Amazon Courtesy Credit?

Amazon Courtesy Credit (ACC) is a form of compensation provided to customers in recognition of various issues or inconveniences they may experience while shopping on the platform. It serves as a gesture of goodwill from Amazon to maintain customer satisfaction and loyalty.

Instances Eligible for Amazon Courtesy Credit

Late Deliveries

Customers may be eligible for ACC if their orders are delivered later than the estimated delivery date provided at the time of purchase.

Damaged or Defective Items

In cases where items arrive damaged or defective, customers can request ACC as a form of compensation for the inconvenience caused.

Inaccurate Product Descriptions

If customers receive items that do not match the product descriptions or specifications listed on the this website, they may qualify for ACC.

How to Request Amazon Courtesy Credit

Customers can request ACC by contacting Amazon customer support and providing details about the issue they encountered. Amazon representatives will assess the situation and determine if compensation is warranted.

Factors Affecting Amazon Courtesy Credit

Customer History and Engagement

Amazon may take into account a customer’s purchase history, order frequency, and overall engagement with the platform when determining eligibility for ACC.

Order Frequency

Frequent and loyal Amazon customers may receive more favorable consideration for courtesy credit compared to occasional shoppers.

Issue Severity

The severity and impact of the issue experienced by the customer also play a role in determining the amount of CC provided.

Benefits of Amazon Courtesy Credit

Amazon Courtesy Credit offers several benefits to customers, including:

- Compensation for inconvenience or dissatisfaction with the shopping experience.

- Enhanced customer satisfaction and loyalty.

- Reinforcement of Amazon’s commitment to customer service excellence.

Limitations and Considerations

While Amazon Courtesy Credit can help address certain issues encountered by customers, it’s important to note that it may not fully compensate for all inconveniences or dissatisfaction experienced during the shopping process.

Customer Experiences and Feedback

Many Amazon customers have shared their experiences and feedback regarding Amazon Courtesy Credit on various online platforms and forums. Exploring these insights can provide valuable perspectives and tips for navigating the process of requesting and utilizing courtesy credit.

Conclusion

It serves as a valuable tool for maintaining customer satisfaction and loyalty by compensating users for certain issues or inconveniences encountered during their shopping experience. By understanding the eligibility criteria and process for requesting courtesy credit, customers can leverage this benefit to enhance their overall shopping experience on Amazon.

FAQs

How do I request ACC for a late delivery?

- To request it for a late delivery, you can contact Amazon customer support through their website or app. Provide details about your order, including the order number and the estimated delivery date. Amazon representatives will assess the situation and may offer compensation in the form of CC.

What should I do if I receive a damaged or defective item from Amazon?

- If you receive a damaged or defective item from Amazon, you should contact Amazon customer support immediately to report the issue. Provide relevant details such as the order number, item description, and images showing the damage or defect. Amazon will assist you in resolving the issue and may offer CC as compensation.

Is ACC provided automatically, or do I need to request it?

- ACC is not provided automatically. You need to request it by contacting Amazon customer support and explaining the issue you encountered. Amazon representatives will evaluate your request and determine if CC is warranted based on their policies and guidelines.

Can I use ACC for future purchases on the platform?

- Yes, ACC can typically be used for future purchases on the Amazon platform. Once credited to your account, CC can be applied towards the payment of eligible items during checkout. However, it’s essential to check the terms and conditions associated with the Courtesy Credit for any specific limitations or restrictions.

Are there any restrictions or limitations on the use of ACC?

- While It can generally be used for purchases on the platform, there may be certain restrictions or limitations depending on the terms and conditions associated with the credit. For example, Courtesy Credit may have an expiration date or be limited to specific categories of products. It’s advisable to review the terms carefully to understand any restrictions before using the Courtesy Credit.

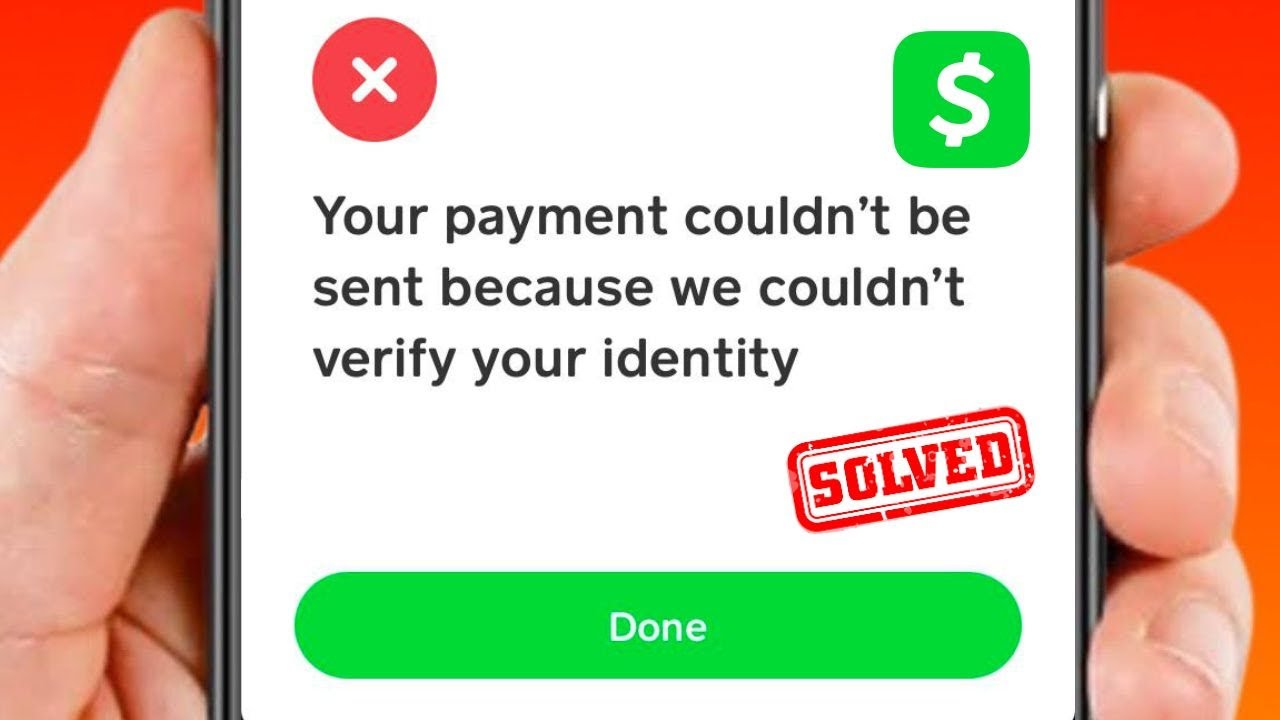

The article “your payment could not be sent cash app” This app emerged as one of the leading mobile payment platforms, offering users a convenient way to send, receive, and manage money directly from their smartphones. While Cash App provides a seamless payment experience for millions of users, occasional issues may arise, leading to payment failures and frustrations for users.

Understanding Payment Issues on Cash App

Payment issues on Cash App can occur due to various reasons, ranging from technical glitches to user error. When your payment cannot be sent on Cash App, it’s essential to understand the underlying causes and take appropriate steps to resolve the issue promptly.

Common Reasons for Payment Failures

Several factors can contribute to payment failures on Cash App, including insufficient funds, incorrect recipient information, network connectivity issues, and security concerns. Identifying the specific reason for the payment failure is crucial for resolving the issue effectively.

Steps to Take When Your Payment Cannot be Sent

If your payment could not be sent on Cash App, consider the following steps to troubleshoot the issue:

Check Account Balance:

- Ensure that you have sufficient funds in your Cash App account to cover the payment amount.

Verify Recipient Information:

- Double-check the recipient’s details, including their Cash App username or phone number, to ensure accuracy.

Retry the Payment:

- Attempt to resend the payment after confirming that all details are correct.

Monitor Transaction Status:

- Keep track of the transaction status within the Cash App interface to receive real-time updates on the payment attempt.

Contact Cash App Support:

- If the issue persists, reach out to Cash App support for assistance and further troubleshooting steps.

Contacting Cash App Support

In case of persistent payment issues, contacting Cash App support is the best course of action. Users can reach out to Cash App customer service through the app or website for personalized assistance and resolution of payment-related concerns.

Tips to Avoid Payment Issues on Cash App

To minimize the risk of payment failures and ensure a smooth transaction experience on Cash App, consider the following tips:

- Maintain Sufficient Funds: Regularly check your Cash App balance and add funds as needed to avoid payment failures due to insufficient funds.

- Verify Recipient Details: Always double-check the recipient’s information before initiating a payment to prevent errors and potential delays.

- Stay Updated: Keep your Cash App and device software up to date to benefit from the latest security patches and enhancements.

- Use Secure Networks: Avoid conducting Cash App transactions over unsecured or public Wi-Fi networks to protect your sensitive information from potential security threats.

Ensuring Account Security

In addition to addressing payment issues, prioritizing account security is paramount when using Cash App. Users should enable two-factor authentication, review transaction history regularly, and report any unauthorized activity promptly to safeguard their accounts and financial information.

Comparing Cash App with Other Payment Platforms

While Cash App offers convenience and flexibility for peer-to-peer payments, it’s essential to compare its features and functionality with other payment platforms. By evaluating factors such as transaction fees, security measures, and user experience, users can make informed decisions about which platform best suits their needs.

Conclusion

In conclusion, encountering payment issues on Cash App can be frustrating, but understanding the underlying causes and taking proactive steps can help resolve the problem effectively. By following best practices for account security, verifying recipient information, and staying informed about transaction status, users can minimize the risk of payment failures and enjoy a seamless payment experience on Cash App.

FAQs

What should I do if my payment fails on Cash App?

- If your payment fails on Cash App, double-check the recipient’s information and account balance before attempting to resend the payment. If the issue persists, contact Cash App support for assistance.

How long does it take for Cash App to resolve payment issues?

- The time taken to resolve payment issues on Cash App varies depending on the nature of the problem. In most cases, Cash App strives to address payment concerns promptly and efficiently.

Can I cancel a failed payment on Cash App?

- Yes, users have the option to cancel a failed payment on Cash App before it is successfully processed. However, once a payment is completed, it cannot be canceled or reversed.

Does Cash App charge a fee for failed payments?

- Cash App does not charge a fee for failed payments. However, standard transaction fees may apply when sending money or using certain features within the app.

Are there any limits on the amount of money I can send through Cash App?

- Cash App imposes certain limits on the amount of money users can send and receive within a specified time frame. These limits may vary based on account verification status and other factors.

Business

Ace Hair Extensions & Co Overtakes other beauty brands with it’s new Serum & XL Ace Lace Glue

A brand receiving strong demands for its services must always continue to listen to their customers on what better ways to serve them, which Ace Hair Extensions & Co did last year which led to the innovations of new skus and items.

They have continued to defie luxury downturn and have continued to see new customer satisfactory reviews on forums and social media blogs alike.

Besides their Glue being #1 on the market for bonding strength, The Parfum Serum is made with different plant and root extracts, revealing natural scents and tones that last all day.

It’s Non oily, very silk-like, smells amazing, and is made from organic properties.

Many owning these beautiful products know how much they mean to Ace Hair Extensions & Co when they receive their packages in the mail and see the stylish packaging and attention to detail so they dress their bathroom counters and dressing tables up with their new luxuries.

Experience greatness again https://acehairextensionsco.com/products/hair-serum?variant=40613161369661

Others10 months ago

Others10 months agoDavid T Bolno: Why Giving Back To The Community Is So Crucial

Travel10 months ago

Travel10 months agoPractical And Essential Car Interior Accessories To Add Comfort And Convenience To Your Drive

Travel10 months ago

Travel10 months agoBusiness Visa for CANADA

Business10 months ago

Business10 months agoTop Reasons Why you Need to Consider Outsourcing Real Estate Photo Editing

Health10 months ago

Health10 months agoGarlic Is The Best Vegetable To Treat Heart Problems

Business10 months ago

Business10 months agoDead And Co Setlist What They Played At The Gorge Amphitheatre

Fashion10 months ago

Fashion10 months agoTips For Choosing The Right For Engagement Diamond Rings

Tech10 months ago

Tech10 months agoThe Best Way to Never Get Lost: Buy Wayfinding Signs!